Applying for quick business loans online can be one of the fastest ways to get the funds your company needs. Whether you’re facing a cash flow gap, planning expansion, or handling unexpected expenses, online lenders offer speed, convenience, and simple qualification requirements. But many business owners make avoidable mistakes during the loan process, and those mistakes can slow down approvals or even lead to rejections. To help you get funded without delays, here are the five most common mistakes to avoid when applying for quick business loans.

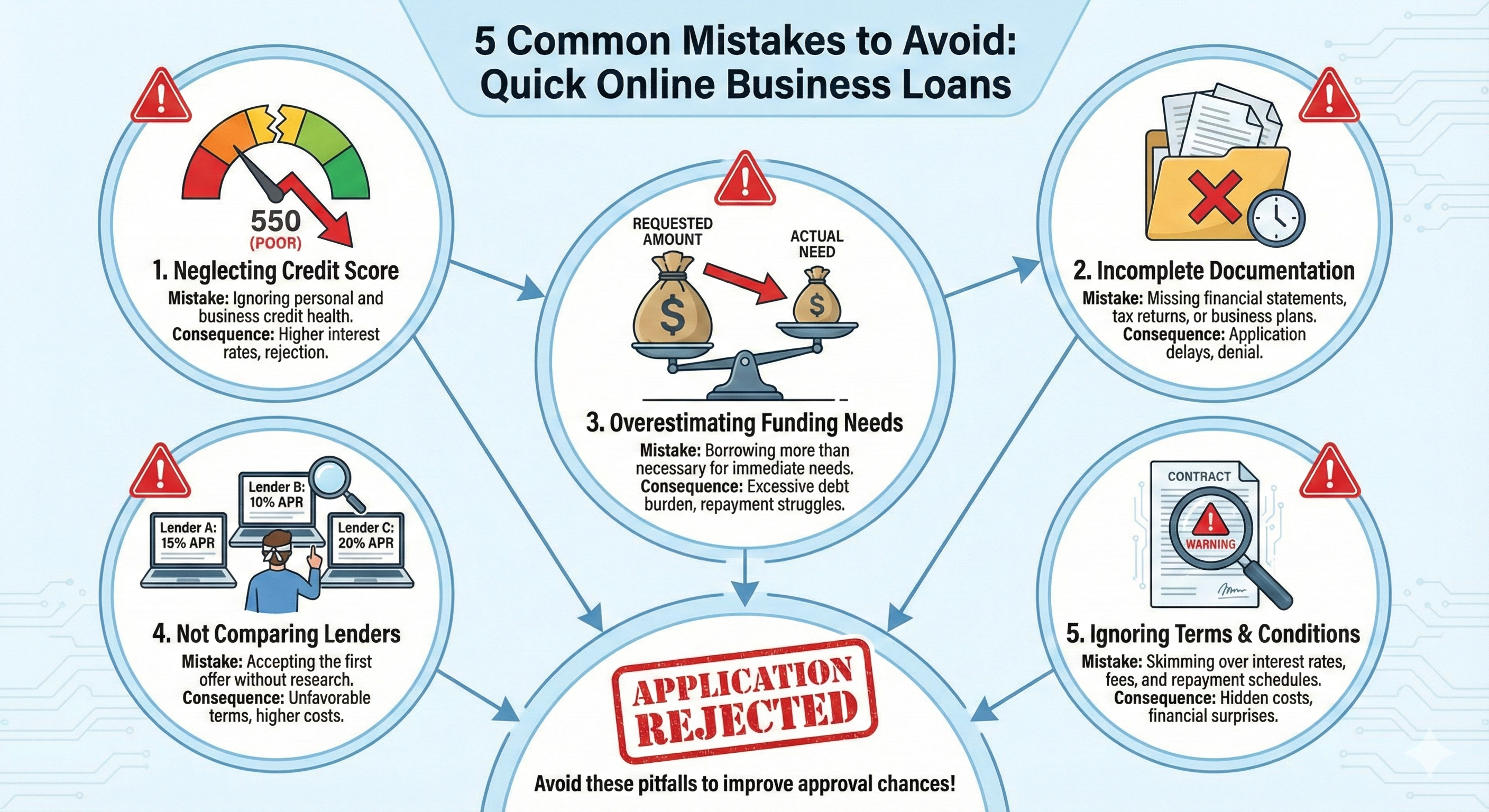

1. Not Checking Your Business’s Financial Health

One of the biggest mistakes is applying without understanding your current financial standing. Online lenders look at your cash flow, monthly revenue, and existing debts. If these numbers are unclear or inconsistent, your approval chances drop.

What to do instead:

Review your bank statements, profit-and-loss reports, and monthly revenue trends before applying. Strong financial clarity helps lenders approve your quick business loan faster and with better terms.

2. Applying Without Comparing Multiple Lenders

Many business owners apply to the first lender they see online. This often leads to higher interest rates or terms that don’t match what the business actually needs.

What to do instead:

Compare at least three lenders offering quick business loans online. Look at their interest rates, fees, repayment terms, and funding timelines. A little research can save you money and help you choose a loan that truly fits your business goals.

3. Providing Incomplete or Incorrect Documents

Missing or incorrect information is one of the main reasons online applications get delayed. When lenders don’t have accurate details, they can’t move forward with approval.

What to do instead:

Prepare your documents in advance. Most lenders require:

- Bank statements (3–6 months)

- Government ID

- Business registration documents

- Basic financials

Clean, correct documentation helps you secure quick business funding without back-and-forth delays.

4. Borrowing More Than You Actually Need

It’s easy to overestimate how much funding your business needs. Many owners apply for higher loan amounts, hoping to secure more flexibility. But larger loan requests often mean stricter approval requirements, higher interest, and increased rejection risk.

What to do instead:

Calculate what your business truly needs for its next step. A realistic loan amount increases your chances of fast approval and keeps repayment manageable.

5. Ignoring the Loan Terms and Hidden Fees

Some business owners focus only on funding speed and overlook important details like interest rates, processing fees, or prepayment penalties. These overlooked costs can add up over time.

What to do instead:

Read the full loan agreement before signing. Understand exactly how much you’ll repay each month and the total cost of borrowing. Choosing transparent lenders ensures your quick business loan supports growth without unexpected expenses.

Final Thoughts

Getting quick business loans online is easier than ever, but avoiding these common mistakes can make the process even smoother. Prepare your financials, compare lenders, share correct information, borrow responsibly, and read all terms carefully. These steps can help you secure fast funding with confidence and clarity.